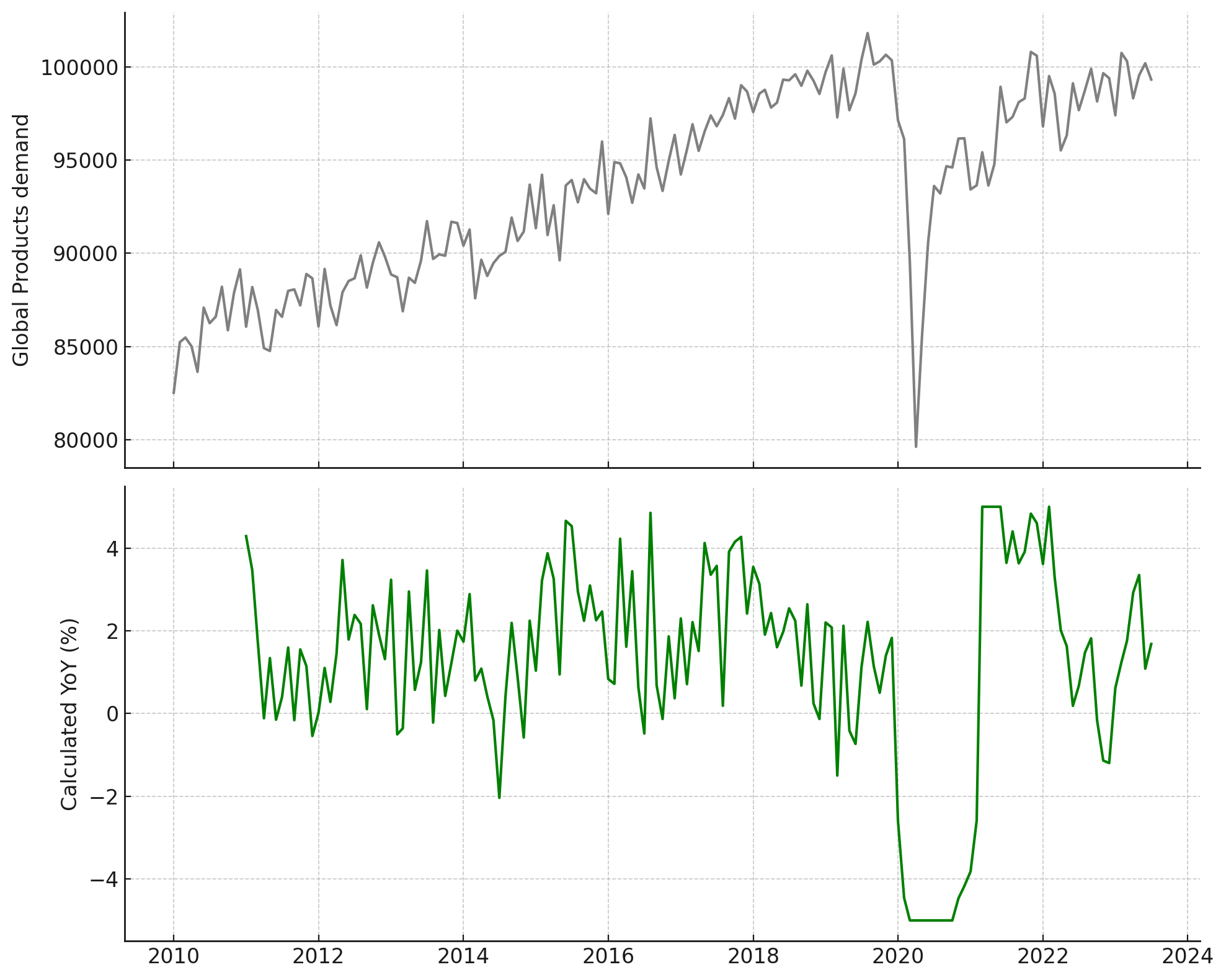

One can see that demand is already rolling over since april-may 23 (extremes YoY measures during covid have been removed in the above chart)

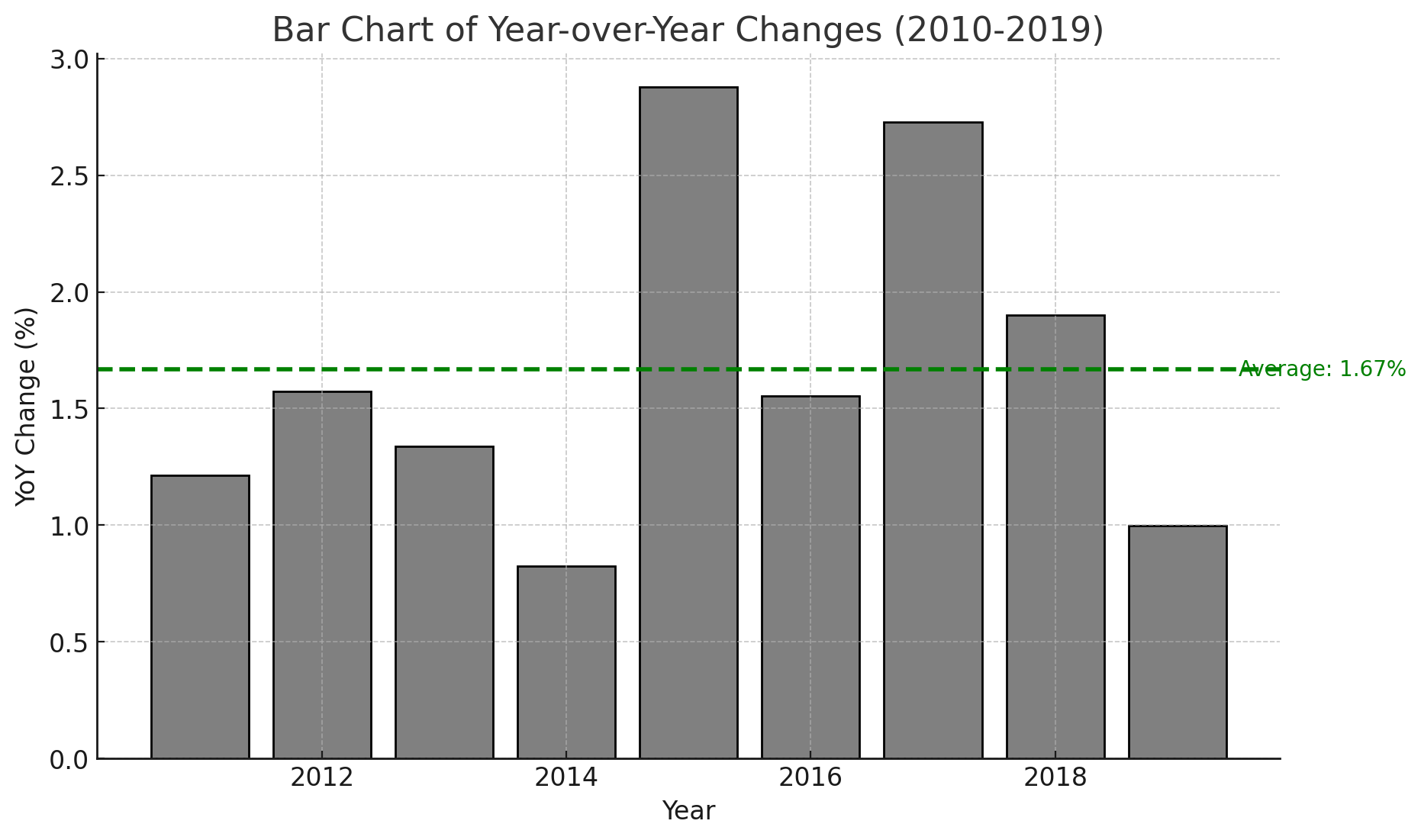

The current YoY demand growth is not significantly different from the average growth of the previous decade (+1.67%). However, the next few months are likely to show that this historical average is a thing of the past. It is possible that normalized demand growth after the COVID-19 pandemic will be half of what it used to be, or even lower.

- China: 18.57%

- Vietnam: 15.66%

- India: 9.23%

- Indonesia: 5.21%

- Portugal: 3.27%

- Thailand: -0.37%

- United States: -1.18%

- Germany: -6.70%

- Mexico: -7.05%

- Turkey: -8.04%

- France: -8.73%

- Nigeria: -9.67%

- Sweden: -12.74%

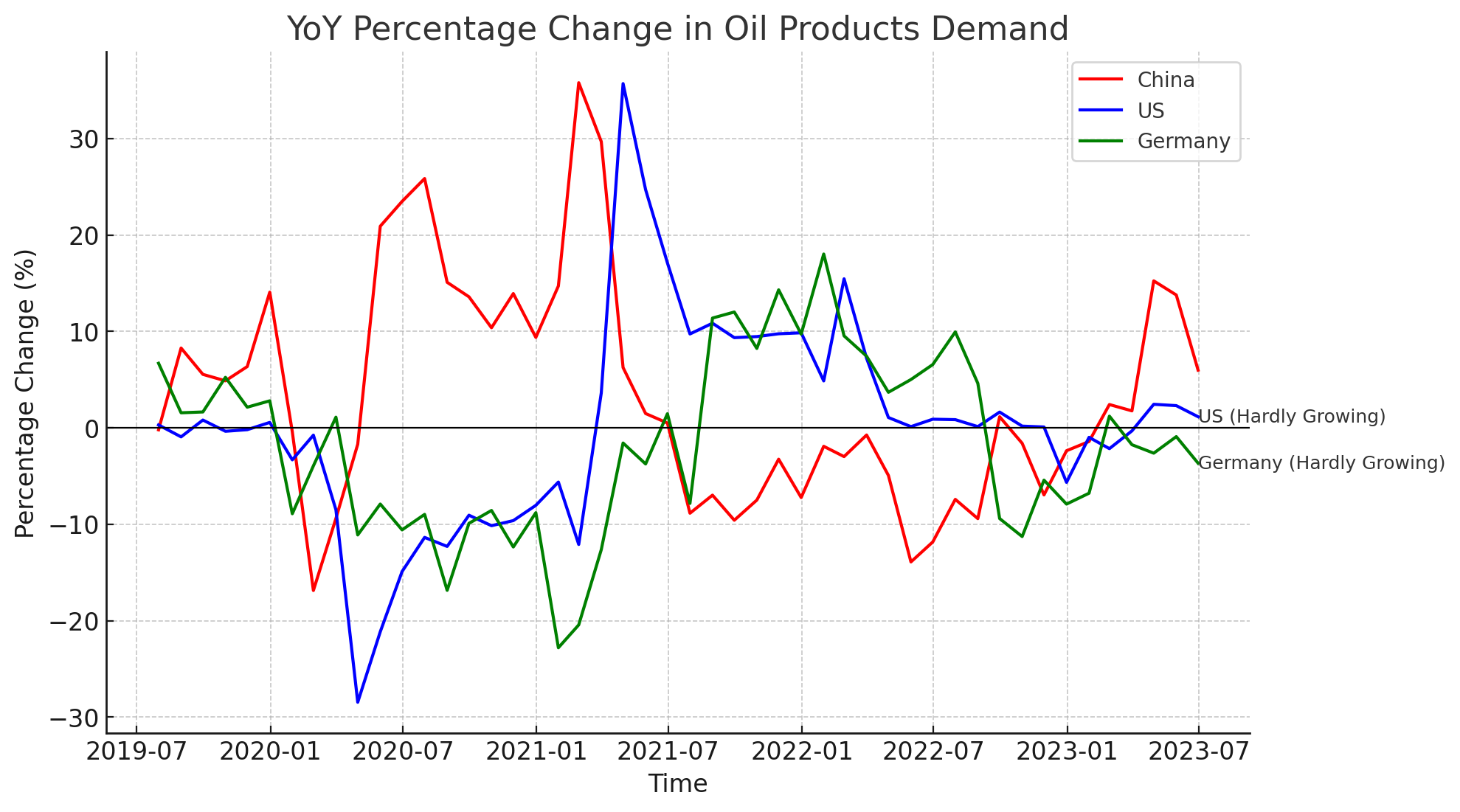

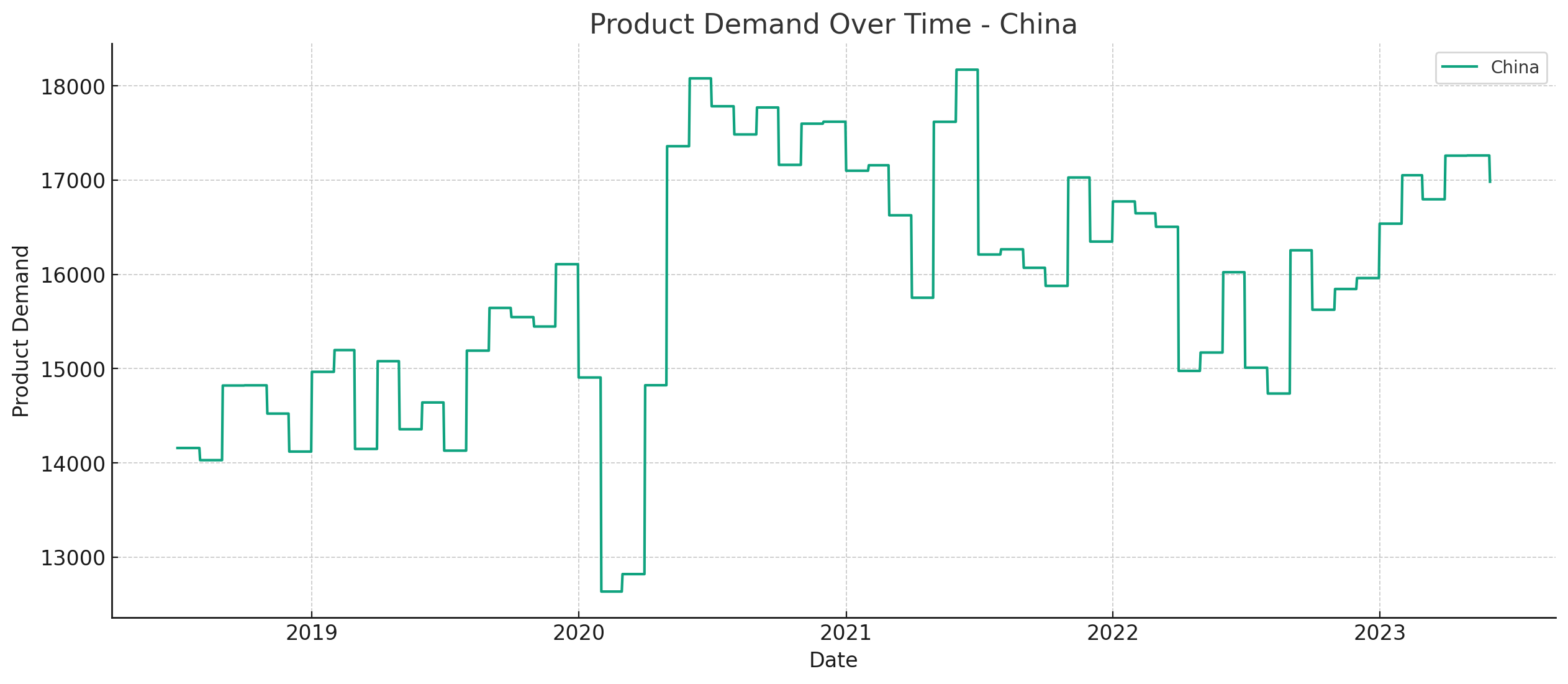

China has been key to final product demand over the past years. Chinese demand growth has stalled during the Covid period though…

End of content

No more pages to load